Recession. The “Big R” of economics. One of the more confounding aspects of the word is that just hearing it can cause people to behave differently. If enough people prepare for a recession by saving more and consuming less, such behavior can bring about the very economic contraction that many people fear. Do recent trends in implied volatility give us any indications that investors are behaving like they have in past recessionary periods?

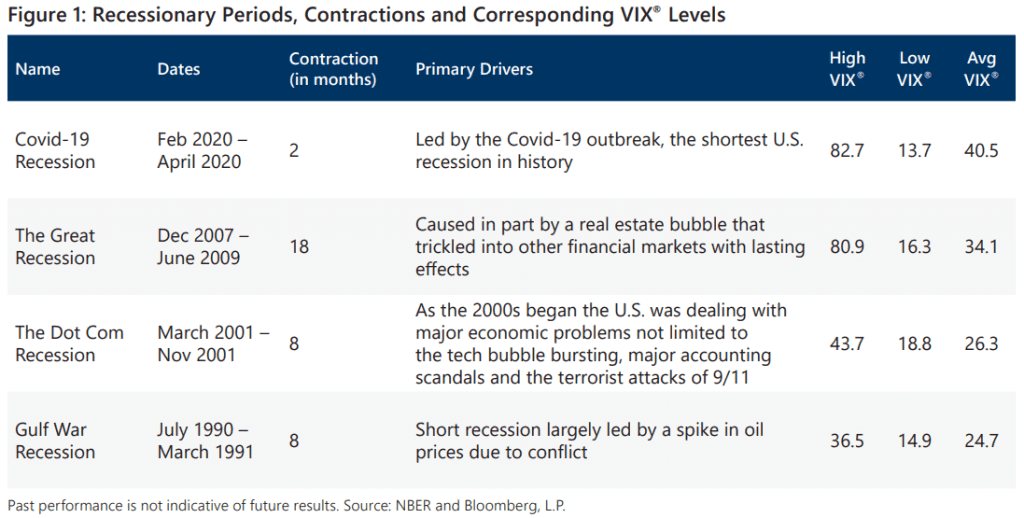

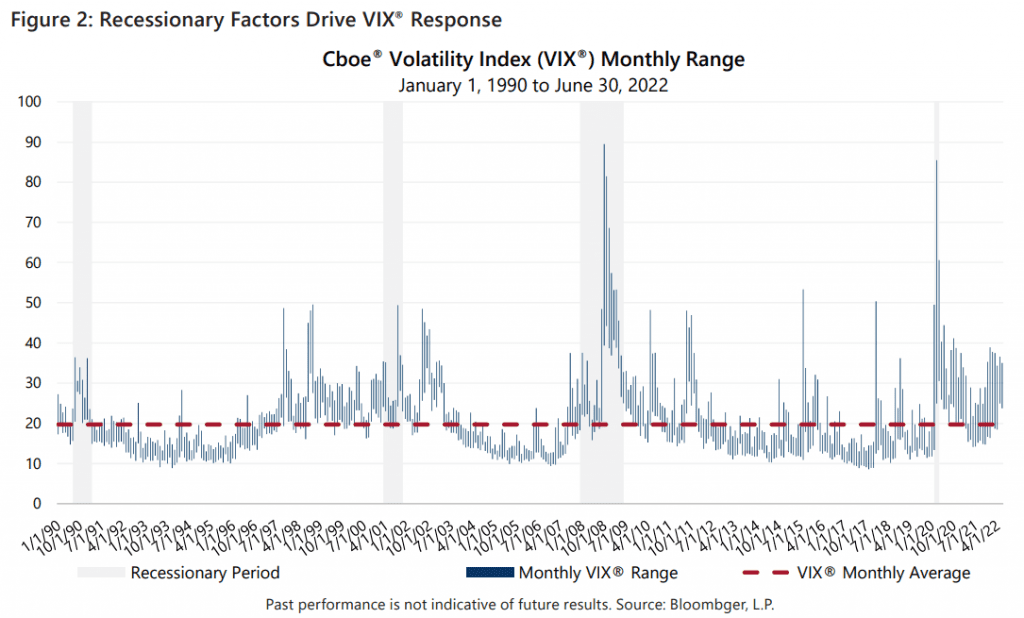

The National Bureau of Economic Research (NBER) has not labeled the current state of the U.S. economy a recession, and it remains to be seen whether the economy deteriorates further or begins to improve as the group makes its determination of where we are in the business cycle. Comparing Cboe® Volatility Index (the VIX®) levels of the last six months to those seen during official NBER recessionary periods going back to the early 1990s shows that the recent six-month average is at the low-end of its range for levels during recessions. Additionally, the recent six-month high for the VIX® is in-line with the lowest VIX® maximum during recessions.

Every recessionary period throughout history has been unique, as has the equity market environment surrounding each of these periods. Figure 1 outlines the length of time, primary drivers and implied volatility levels of recent recessionary periods which show the difference between each period. The current equity market is no exception. In fact, after posting two consecutive quarters of declining GDP and in the face of record and rising inflation, tightening monetary policy and ongoing geopolitical uncertainty (to name just a few headwinds), the S&P 500® Index had its best monthly return since November 2020 and its best July since 1989!

So, does investor behavior predict market moves or provide any insight for the future? While Gateway avoids predictions, data on open interest for index put options over the recent past show that the level of purchased protection was nearly 20% higher in December 2021 than it was in December 2020. Investors may not have known which path the market would take, but a significant number were more comfortable owning protection than not.

For investors concerned that the economy or capital market conditions may deteriorate further in the months ahead, managing risk with strategies that generate cash flow from option writing may have benefits relative to managing risk with bonds in an inflationary environment. For investors who feel that the economic slowdown in the first half of 2022 was temporary and conditions will improve, index option-based low volatility equity strategies may offer more return potential, with a similar risk profile as fixed income investments. Since 1977, Gateway has provided access to the unique potential of option strategies, helping investors navigate an array of unique equity and bond market environments.

Past performance is no guarantee of future results.

For more information and access to additional insights from Gateway Investment Advisers, LLC, please visit www.gia.com/insights.