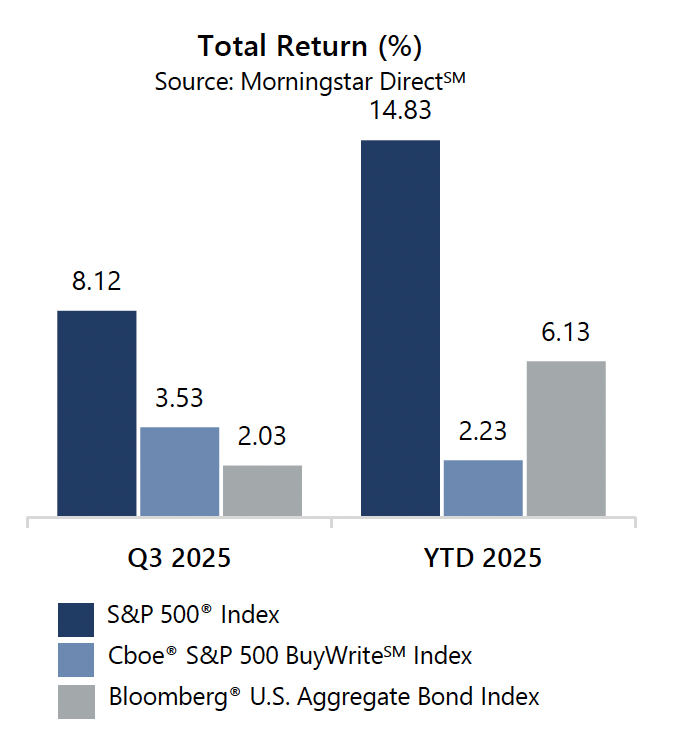

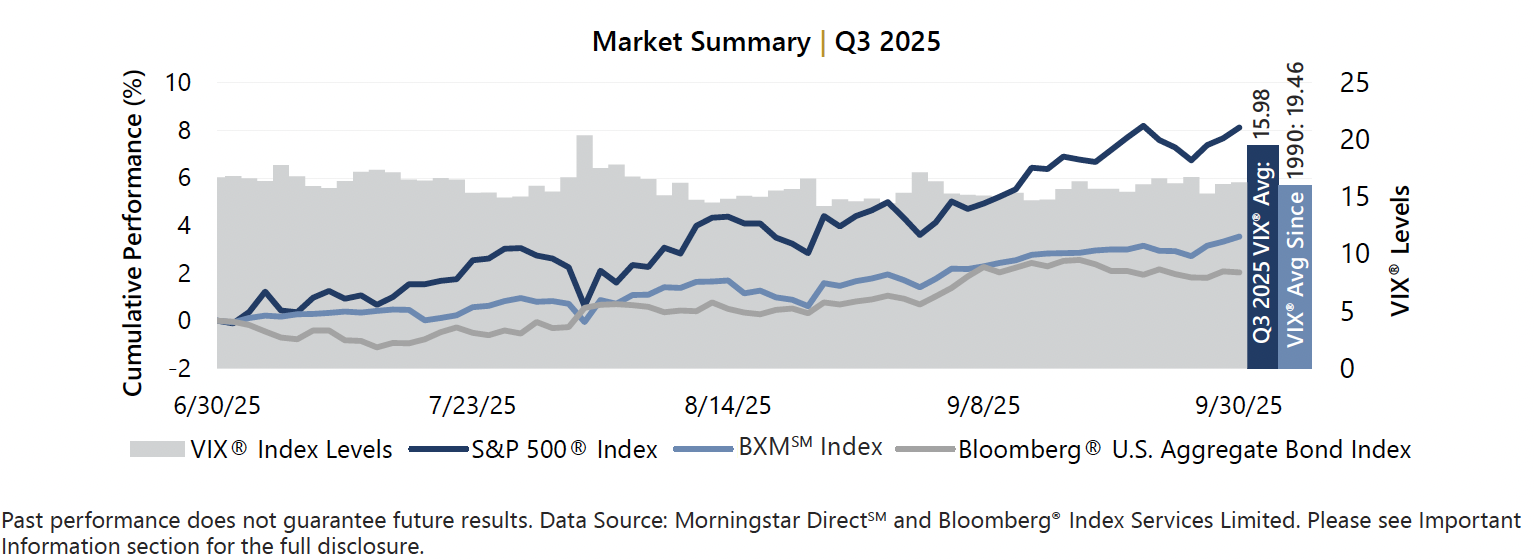

The S&P 500® Index advanced 8.12% during the third quarter of 2025, bringing its year-to-date return to 14.83%. With the tariff tantrum in the rearview mirror and the expectation of additional interest rate cuts in 2025, the S&P 500® Index reached a new all-time high on September 22 before closing its best September since 2010. The S&P 500® Index started the quarter relatively muted, climbing just 0.61% from the close of the second quarter to August 1. As the Federal Reserve began warming to the idea of an interest rate cut, the equity market advance accelerated. From August 1 through quarter-end, the S&P 500® Index advanced 7.47%.

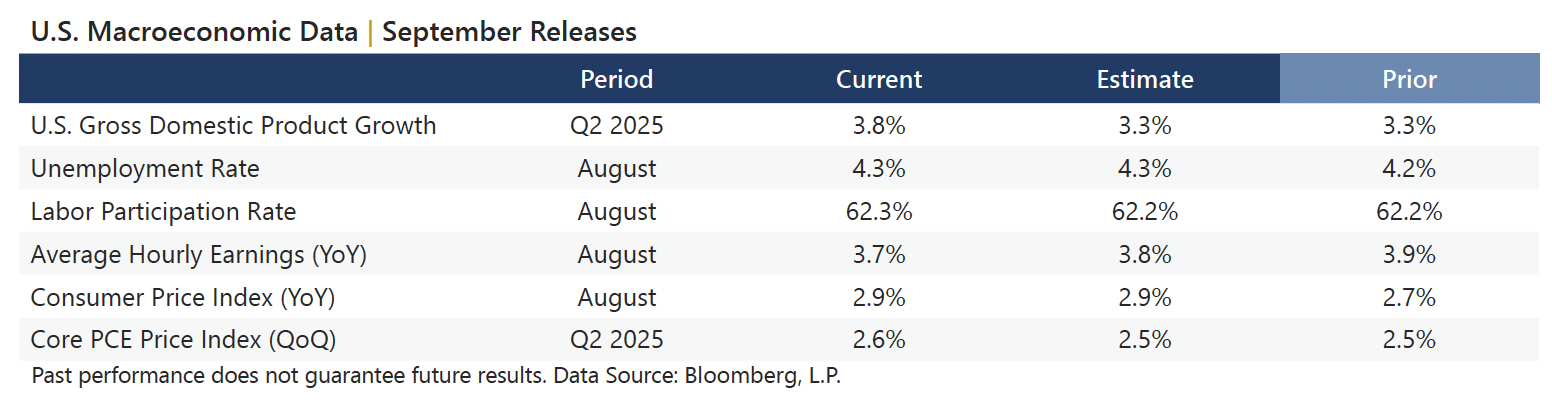

Data released in September reflected continued macroeconomic resilience with signs of steady inflation and a steady labor market. The current estimate of Gross Domestic Product for the second quarter of 2025 was increased from the prior estimate and was better than consensus expectations. The year-over-year August Consumer Price Index, released September 11, was in line with the consensus estimate and slightly higher than the prior period. The quarter-over-quarter Personal Consumption Expenditures (PCE) Price Index was higher than the consensus estimate and prior period. With nearly all S&P 500® Index companies reporting, corporate earnings are on track to be positive for the second quarter of 2025. Aggregate operating earnings increased 2.4% quarter-over-quarter and 10.4% year-over-year. More than 83% of reporting companies either met or exceeded analyst estimates.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 3.53% in the third quarter, bringing its year-to-date return to 2.23%. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premiums the BXMSM collected as a percentage of the BXMSM’s underlying value were 1.60%, 1.61%, and 1.54% in July, August, and September, respectively. The rules-based timing of the BXMSM’s option writing and the level of premiums collected as a percentage of its underlying value contribute significantly to the BXMSM’s participation in periods of advance and its level of loss mitigation during periods of market decline.

The Bloomberg® U.S. Aggregate Bond Index returned 2.03% in the third quarter, bringing its year-to-date return to 6.13%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended June at 4.23%, and hit an intra-quarter low of 4.02% on September 11 after touching an intra-quarter high of 4.48% on July 15. The 10-year ended the quarter at 4.15%.