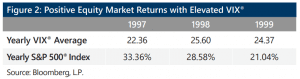

It is important to note that, even though implied volatility tends to rise when the equity market falls, persistently elevated implied volatility does not necessarily equate to persistently falling equity markets. As the table in Figure 2 shows, the late 1990s saw three consecutive years of elevated VIX® averages combined with very attractive equity market returns.

It is important to note that, even though implied volatility tends to rise when the equity market falls, persistently elevated implied volatility does not necessarily equate to persistently falling equity markets. As the table in Figure 2 shows, the late 1990s saw three consecutive years of elevated VIX® averages combined with very attractive equity market returns.

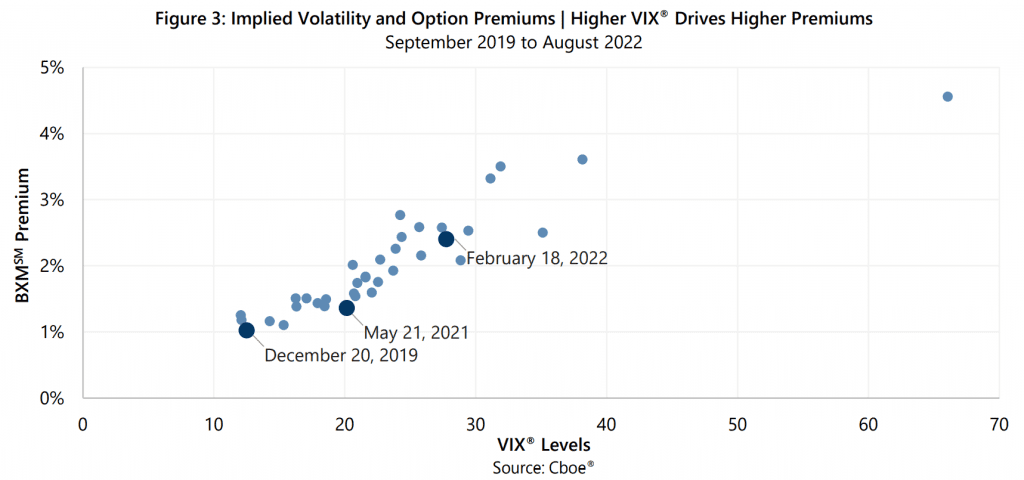

If VIX® levels are not reliable indicators of market direction, how can implied volatility help investors manage risk? Higher implied volatility creates higher index option prices. Writing index options generates cash flow that has a positive relationship with implied volatility – higher VIX® levels result in greater amounts of cash flow from index option writing. Strategies that combine equity market exposure with option writing cash flow can benefit from elevated VIX® levels through potentially improved outcomes in both up-market and down-market scenarios. Figure 3 illustrates the relationship between the VIX® level and the monthly call-writing premiums generated by the Cboe® S&P 500 BuyWrite Index (the BXMSM) over the last 36 months, which covers a representative sample of VIX’s® historical range. When the VIX® is close to its historical average level, as it was on May 21, 2021 when it closed at 20.15, a strategy that writes one-month at-the-money options may receive a premium similar to the 1.36% (note: monthly premium amounts are not annualized) that the BXMSM received on that day. On days with higher VIX® levels, premiums will be higher. For example, the VIX® closed at 27.75 on February 18, 2022 and the BXMSM received a premium of 2.40%. Conversely, lower VIX® results in lower premiums and less cash flow for option writing strategies, such as when the VIX® closed at 12.51 on December 20, 2019 and the BXMSM received a premium of 1.02%.