Given the bond market’s recent propensity to deliver losses with higher frequency and higher correlation to equity market losses, investors who seek a smoother ride than the equity market may be looking for alternatives to bonds for risk reduction – especially since the total return potential of bond portfolios remains relatively low as yields on intermediate- to long-term bonds remain at levels that would accurately be described as “historically low” at any point in history outside of the past 10 years.

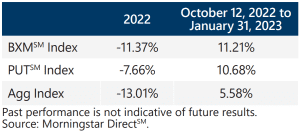

Index option-writing strategies with a low volatility profile may be compelling alternatives. For example, the Cboe® S&P 500 BuyWriteSM Index (the BXMSM) and the Cboe® S&P 500 PutWriteSM Index (the PUTSM) posted smaller losses than both the S&P 500® Index and the Bloomberg U.S. Aggregate Bond Index (the Agg) in 2022. Moreover, the BXMSM and the PUTSM have both generated much higher returns than the Agg since the equity market put in its 2022 low on October 12.

Index option-writing strategies with a low volatility profile may be compelling alternatives. For example, the Cboe® S&P 500 BuyWriteSM Index (the BXMSM) and the Cboe® S&P 500 PutWriteSM Index (the PUTSM) posted smaller losses than both the S&P 500® Index and the Bloomberg U.S. Aggregate Bond Index (the Agg) in 2022. Moreover, the BXMSM and the PUTSM have both generated much higher returns than the Agg since the equity market put in its 2022 low on October 12.

Utilizing index options for risk reduction and risk-adjusted return enhancement may appeal to risk-averse long-term investors who are no longer satisfied with what the bond market has to offer. Low-volatility equity strategies that rely on cash flow from index option selling to both mitigate equity market losses as well as participate in equity market advances, like those managed by Gateway since 1977, may be a suitable alternative for investors who want to reduce their exposure to bonds without increasing overall portfolio risk.