The S&P 500® Index returned 7.56% in the fourth quarter, bringing its calendar year return to -18.11%. With monthly returns of 8.10%, 5.59% and -5.76% in October, November and December, respectively, the strong rally that began the quarter was partially undone by the year’s final meeting of the Federal Reserve (the Fed). The Fed failed to deliver all the gifts on investors’ wish lists, as hopes for a full pivot in policy and rhetoric were not fulfilled. The Fed slowed its pace of tightening with a 50-basis point (bp) hike but offered no change from its relentlessly hawkish rhetoric. This spoiled the positive sentiment that fueled the market advance from the 2022 market low established on October 12. From the year-to-date low set on October 12 through quarter end, the S&P 500® Index climbed 7.76%. The equity market has declined 18.63% from its 2022 high set on January 3.

Data released in December showed an expanding U.S. economy and stable labor market despite persistently high inflation. The third estimate of Gross Domestic Product for the third quarter of 2022 showed that the U.S. grew at an annualized rate of 3.2%, outpacing the consensus expectation. The November unemployment rate held at 3.7%, in line with consensus expectation, while the participation rate ticked down to 62.1%. The November Consumer Price Index, released December 13, showed slight reprieve with a year-over-year increase of 7.1%, which was slightly lower than the consensus expectation. Third quarter aggregate operating earnings were on track to decline 0.8% quarter-over-quarter while increasing over 7% year-over-year. With more than 98% of S&P 500® Index companies reporting, nearly 75% met or exceeded analyst estimates.

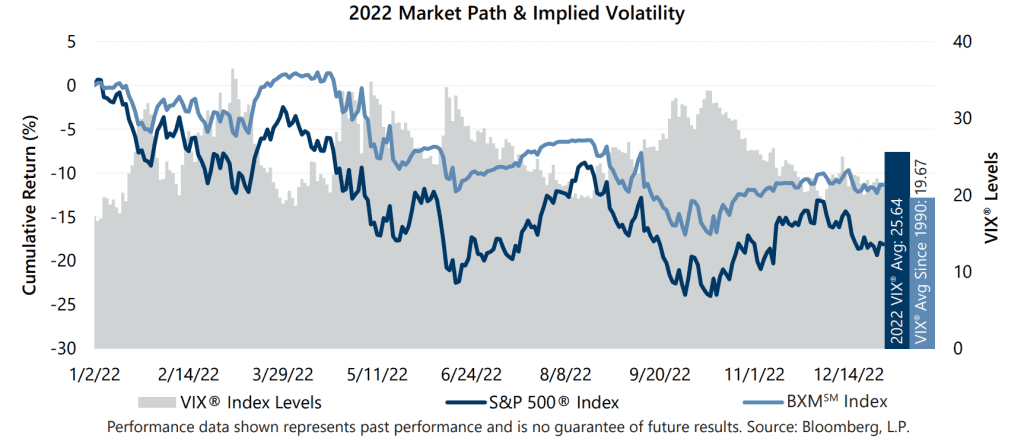

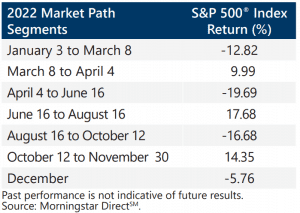

2022 ranks as the fourth worst performing year for the S&P 500® Index over the last 85 years, ranking just below the 2002 decline of -22.10%. The fourth quarter’s Fed-driven rally and selloff was emblematic of a tumultuous year driven by concerns over inflation and monetary policy. The year began with three consecutive losing quarters as the S&P 500® Index returned -4.60%, -16.10% and -4.88% in the first, second and third quarters, respectively. The quarterly returns suggest an incessant market slide followed by a fourth quarter rally. However, the equity market path was more roller coaster than avalanche, as the first three quarters featured double-digit drawdowns and the last two quarters featured double-digit rallies that resulted in only partial recoveries. Concerns over the pace and extent of monetary tightening were a key driver of each market decline while rallies were mostly ignited by investor hopes of a Fed pivot towards less hawkish, if not dovish, approach to achieving lower inflation without tipping the economy into recession.

2022 ranks as the fourth worst performing year for the S&P 500® Index over the last 85 years, ranking just below the 2002 decline of -22.10%. The fourth quarter’s Fed-driven rally and selloff was emblematic of a tumultuous year driven by concerns over inflation and monetary policy. The year began with three consecutive losing quarters as the S&P 500® Index returned -4.60%, -16.10% and -4.88% in the first, second and third quarters, respectively. The quarterly returns suggest an incessant market slide followed by a fourth quarter rally. However, the equity market path was more roller coaster than avalanche, as the first three quarters featured double-digit drawdowns and the last two quarters featured double-digit rallies that resulted in only partial recoveries. Concerns over the pace and extent of monetary tightening were a key driver of each market decline while rallies were mostly ignited by investor hopes of a Fed pivot towards less hawkish, if not dovish, approach to achieving lower inflation without tipping the economy into recession.