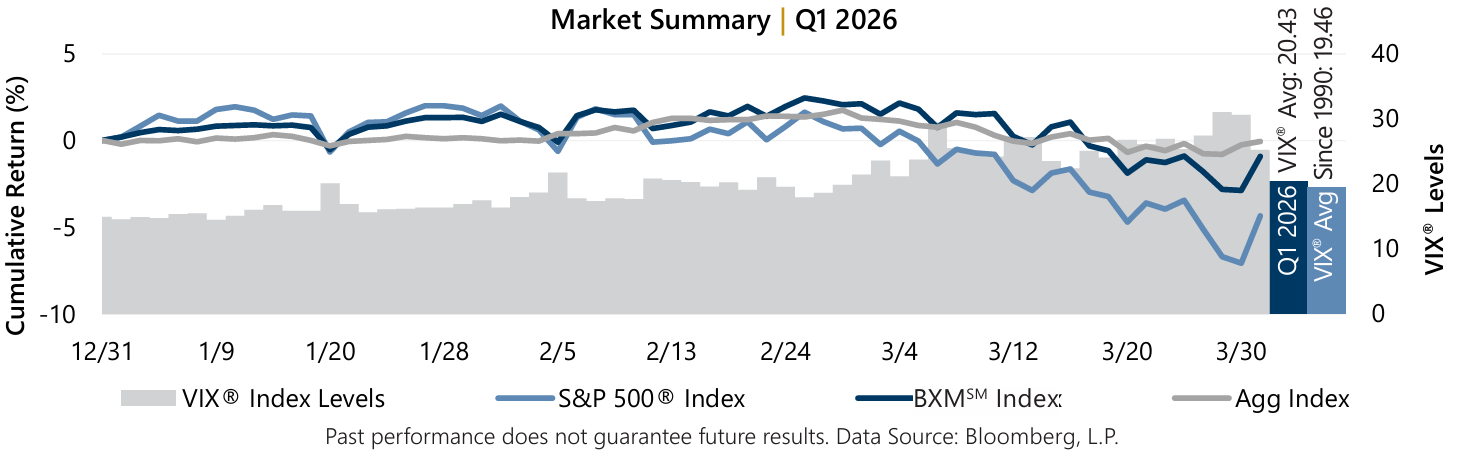

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -0.92% in the first quarter. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premiums the BXMSM collected as a percentage of the BXMSM‘s underlying value were 1.75%, 1.66%, and 2.57% in January, February, and March, respectively. The rules-based timing of the BXMSM‘s replacement of its single written index call option contract resulted in the BXMSM having varied levels of market exposure.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -0.92% in the first quarter. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premiums the BXMSM collected as a percentage of the BXMSM‘s underlying value were 1.75%, 1.66%, and 2.57% in January, February, and March, respectively. The rules-based timing of the BXMSM‘s replacement of its single written index call option contract resulted in the BXMSM having varied levels of market exposure.

The Bloomberg® U.S. Aggregate Bond Index returned -0.05% in the first quarter. The yield on the 10-year U.S. Treasury Note (the 10-year) ended December at 4.17% and hit an intra-quarter low of 3.94% on February 27 before climbing to an intra-quarter high of 4.43% on March 27. The 10-year ended the quarter at 4.32%.