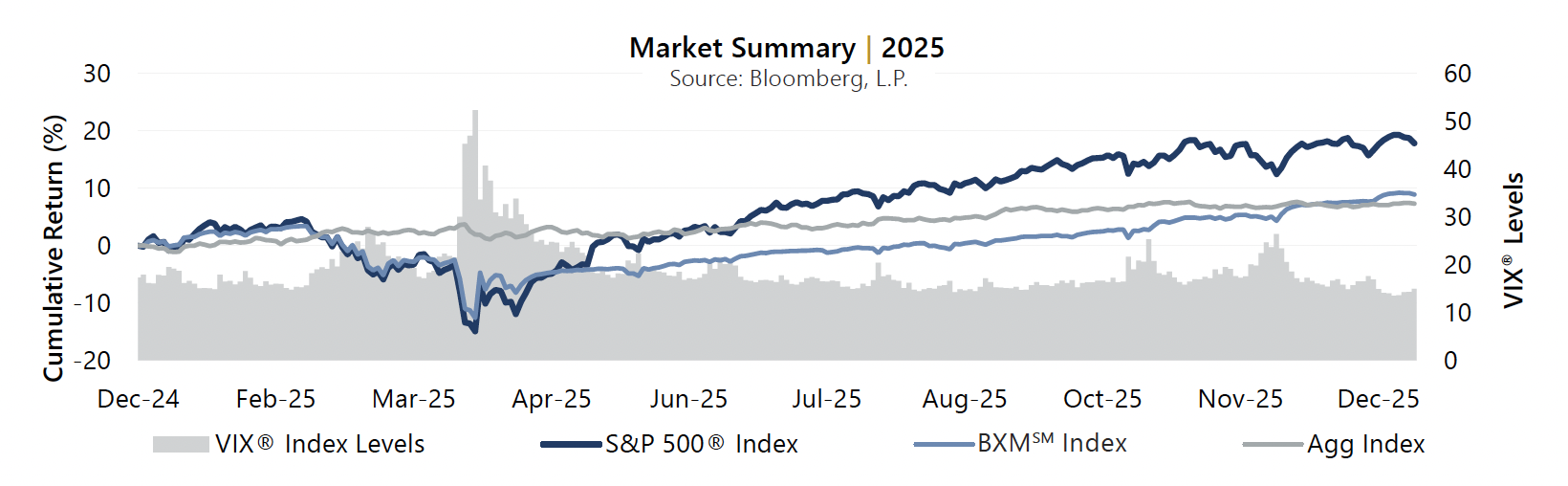

The quarterly spread between S&P 500® Index implied and realized volatility, or the Volatility Risk Premium, was 5.14% – well above the since-1990 average of 3.57%. Implied volatility, as measured by the VIX®, averaged 17.75 in the fourth quarter. Consistent with its typical relationship, average implied volatility exceeded realized volatility, as measured by the standard deviation of daily returns for the S&P 500® Index, which was 12.61% for the quarter. The VIX® ended the third quarter at 16.28 before reaching an intra-quarter high of 26.42 on November 20. As the U.S. government reopened and the market advanced, the VIX® retreated to an intra-quarter low of 13.47 on December 24 before ending the quarter at 14.95.

The quarterly spread between S&P 500® Index implied and realized volatility, or the Volatility Risk Premium, was 5.14% – well above the since-1990 average of 3.57%. Implied volatility, as measured by the VIX®, averaged 17.75 in the fourth quarter. Consistent with its typical relationship, average implied volatility exceeded realized volatility, as measured by the standard deviation of daily returns for the S&P 500® Index, which was 12.61% for the quarter. The VIX® ended the third quarter at 16.28 before reaching an intra-quarter high of 26.42 on November 20. As the U.S. government reopened and the market advanced, the VIX® retreated to an intra-quarter low of 13.47 on December 24 before ending the quarter at 14.95.The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 6.53% in the fourth quarter and 8.91% during the full year. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premiums the BXMSM collected as a percentage of the BXMSM’s underlying value were 2.60%, 2.92%, and 1.59% in October, November, and December, respectively. The rules-based timing of the BXMSM’s option writing and the level of premiums collected as a percentage of its underlying value contributed significantly to the BXMSM’s participation in periods of advance and its level of loss mitigation during periods of market decline.

The Bloomberg® U.S. Aggregate Bond Index returned 1.10% in the fourth quarter, bringing its full year return to 7.30%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended September at 4.15% and hit an intra-quarter low of 3.95% on October 22 before climbing to an intra-quarter high of 4.19% on December 9. The 10-year ended the quarter at 4.17%.