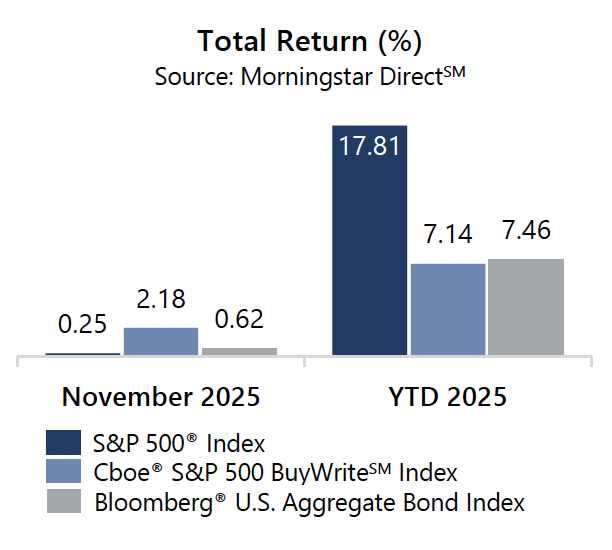

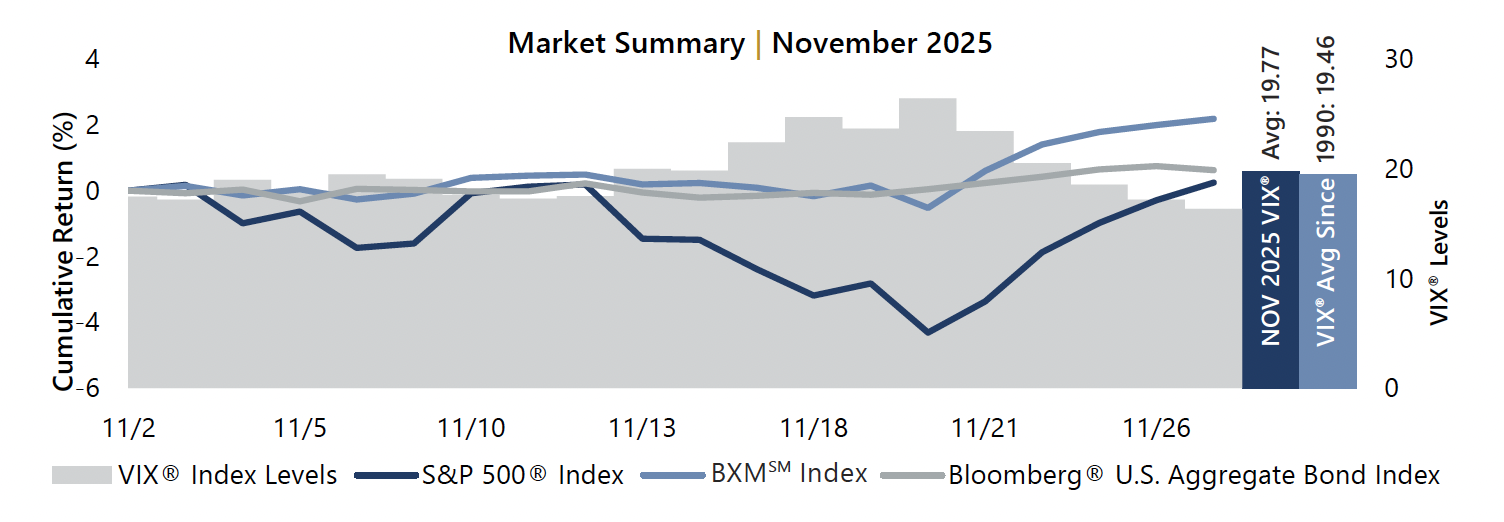

The slightly positive return of the S&P 500® Index during November masked a volatile month. After advancing 0.19% from the start of the month through November 12, the market declined 4.50% from November 12 to November 20 before rallying 4.77% through month-end. The mid-month drawdown was driven by concerns surrounding stretched equity market valuations, especially in leading technology and artificial intelligence related companies. The late-month rally was boosted by growing expectations of another interest rate cut in December.

The slightly positive return of the S&P 500® Index during November masked a volatile month. After advancing 0.19% from the start of the month through November 12, the market declined 4.50% from November 12 to November 20 before rallying 4.77% through month-end. The mid-month drawdown was driven by concerns surrounding stretched equity market valuations, especially in leading technology and artificial intelligence related companies. The late-month rally was boosted by growing expectations of another interest rate cut in December.

With nearly all S&P 500® Index companies reporting, corporate earnings are on track to be positive for the third quarter of 2025. Aggregate operating earnings increased 5.5% quarter-over-quarter and 12.9% year-over-year. More than 85% of reporting companies either met or exceeded analyst estimates.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 2.18% in November, bringing its year-to-date return to 7.14%. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premium the BXMSM collected as a percentage of its underlying value was 2.92% in November. The rules-based timing of the BXMSM’s option writing and the level of premiums collected as a percentage of its underlying value contributed significantly to the BXMSM’s participation in periods of advance and its level of loss mitigation during periods of market decline.

The Bloomberg® U.S. Aggregate Bond Index returned 0.62% in November, bringing its year-to-date return to 7.46%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended October at 4.08% and hit an intra-month high of 4.16% on November 5 before reaching an intra-month low of 3.99% on November 26. The 10-year ended the month at 4.01%.