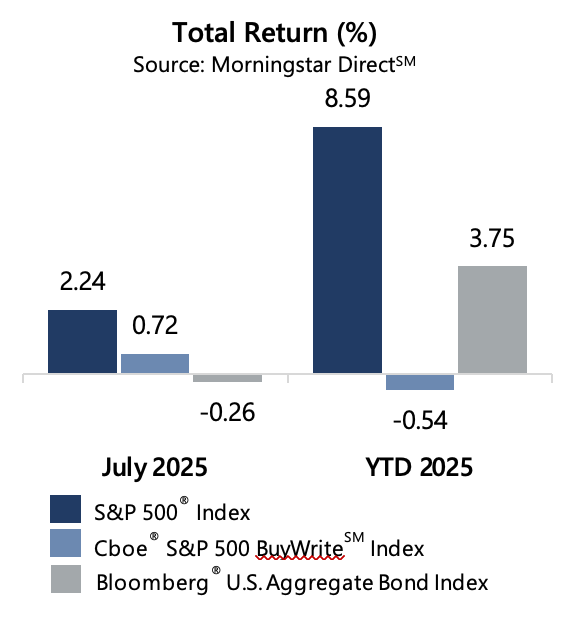

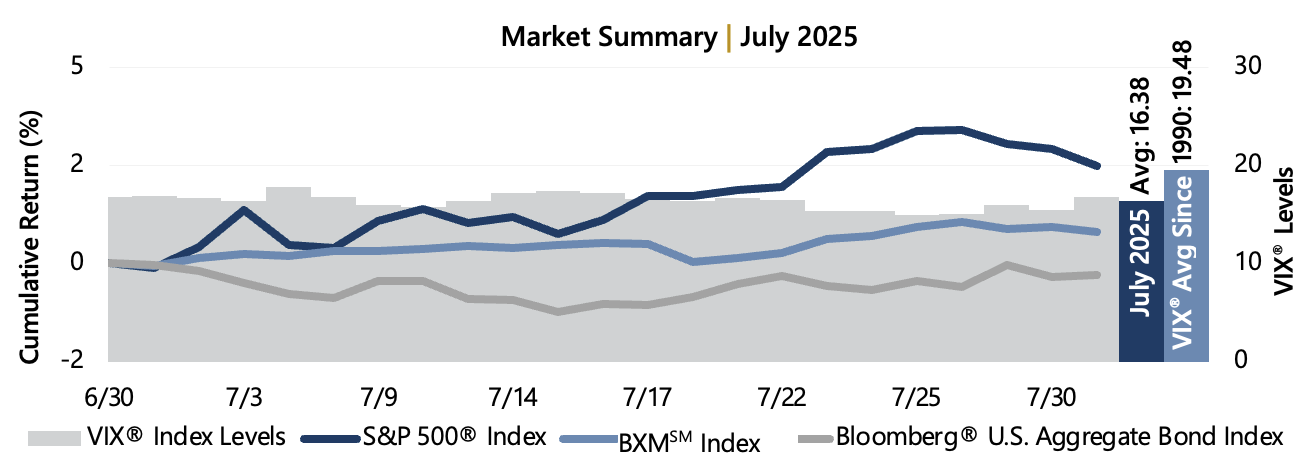

The S&P 500® Index continued its march higher with a 2.24% return in July, bringing its year-to-date return to 8.59%. The S&P 500® Index reached a new all-time high on July 28 before settling the month slightly lower. Investors remained focused on evolving trade negotiations, the health of the U.S. economy, and the direction of the U.S. Federal Reserve who decided to once again hold interest rates steady at their July 30 meeting.

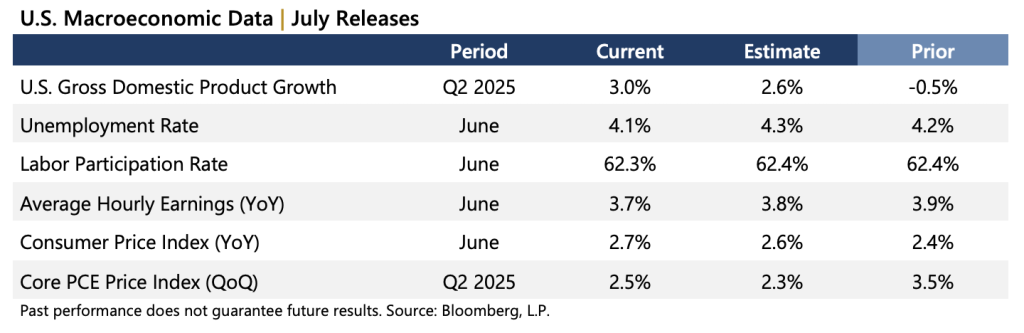

Data released in July reflected a resilient economic backdrop with a steady labor market and inflationary environment. The current estimate of Gross Domestic Product for the second quarter of 2025 was an improvement from the first quarter and better than consensus expectations. The year-over-year June Consumer Price Index, released July 15, was higher than consensus estimates and the prior period. The quarter-over-quarter Personal Consumption Expenditures (PCE) Price Index dipped below the prior month figure and was above estimates. With nearly 63% of S&P 500® Index companies reporting, corporate earnings are on track to be positive for the second quarter of 2025. Aggregate operating earnings increased 2.1% quarter-over-quarter and 10.1% year-over-year. More than 84% of reporting companies either met or exceeded analyst estimates.

The Cboe® S&P 500 BuyWriteSM Index[1] (the BXMSM) returned 0.72% in July, bringing its year-to-date return to -0.54%. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. The premium the BXMSM collected as a percentage of the BXM’sSM underlying value was 1.60% in July. The rules-based timing of the BXMSM’s option writing and the level of premiums collected as a percentage of its underlying value contributed significantly to the BXMSM’s participation in periods of advance and level of loss mitigation during periods of market decline.

The Bloomberg® U.S. Aggregate Bond Index returned -0.26% in July, bringing its year-to-date return to 3.75%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended June at 4.23% and reached an intra-month low of 4.24% on July 1 before touching an intra-month high of 4.48% on July 15. The 10-year ended the month at 4.37%.