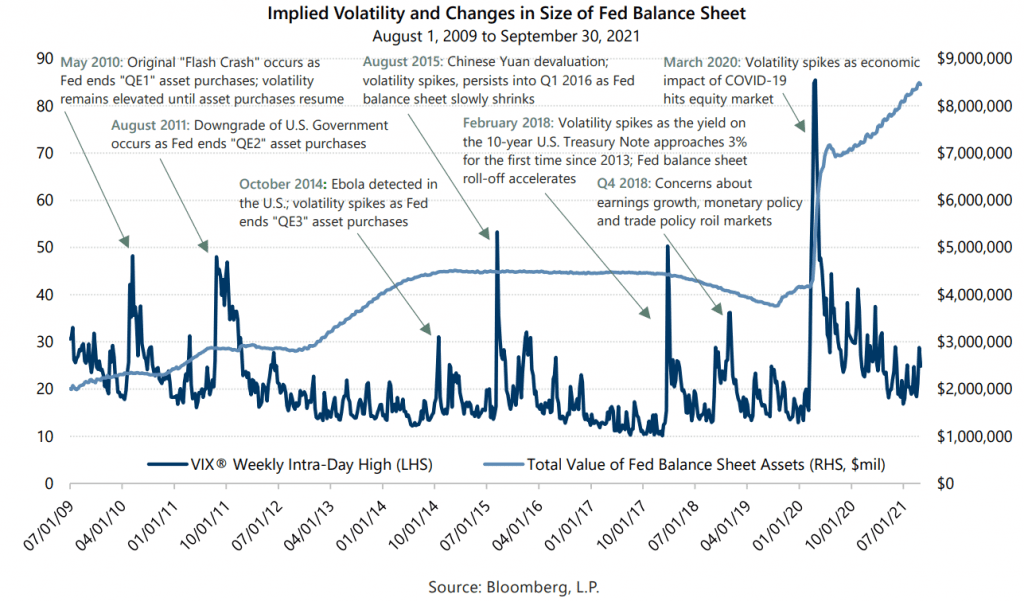

Implied volatility, as measured by the Cboe® Volatility Index (the VIX®), rose in September as investors processed a laundry list of concerns including coronavirus variants, inflation and U.S. political dysfunction. At the press conference after the Federal Open Market Committee (FOMC) on September 22, Chairman Powell indicated that the FOMC was keeping close watch on how economic and financial conditions may be impacted by such concerns, among others. He also indicated the likelihood of a FOMC decision in the near-term that may have a lasting impact on volatility. Chairman Powell noted that recent inflation and employment measures “all but met” the substantial progress tests needed to begin tapering of asset purchases and that the decision to taper may come as soon as the FOMC’s next meeting. The historical relationship between implied volatility and changes in the growth rate of the Federal Reserve’s (the Fed’s) balance sheet shows that the market was more susceptible to elevated volatility in response to adverse events when the Fed was not actively purchasing assets.

As the chart above shows, implied volatility has generally declined or remained below its long-term average of approximately 20 during periods of balance sheet growth through multiple quantitative easing asset purchase programs. Conversely, implied volatility has been relatively elevated during periods when the balance sheet size plateaus or decreases. Furthermore, multiple volatility spikes have coincided with quantitative easing programs coming to an end. The implication of this connection is not that changes in the Fed’s balance sheet caused changes in implied volatility, rather it appears that the market was more susceptible to elevated volatility in response to adverse events during periods when the Fed was not actively purchasing assets.

It remains to be seen whether the historical relationship between implied volatility and changes in the size of the Fed’s balance sheet will continue. However, we believe that investor anxiety over changes to Fed policies, including both interest rate policy and asset purchase policy, is on the list of phenomena that have the potential to keep implied volatility relatively elevated for the remainder of the year.

With interest rates trending up, but still low by historical standards, and amidst a growing number of threats to the equity market’s advance, investment strategies that combine equity market exposure with cash flow from writing index options may have increased appeal for investors seeking long-term return with lower risk than the equity market. Higher implied volatility has the potential to result in higher cash flows from index option writing which, in turn, may improve such strategies’ return potential if the equity market climbs, while also enhancing their potential downside protection if the equity market declines. Conversely, if higher implied volatility trends lower, index option-based low volatility equity strategies may continue to be a compelling alternative to fixed income investments that have reduced return potential in a low to rising interest rate environment.

Gateway’s investment philosophy holds that consistency is the key to long-term investment success and that generating cash flow, rather than seeking to forecast the rise and fall of the market, can be a lower risk means to participate in equity markets. As always, Gateway will look for opportunities to take advantage of the current environment while vigilantly preparing to take appropriate action should conditions change.

*For more information and access to additional insights from Gateway Investment Advisers, LLC, please visit www.gia.com/insights.