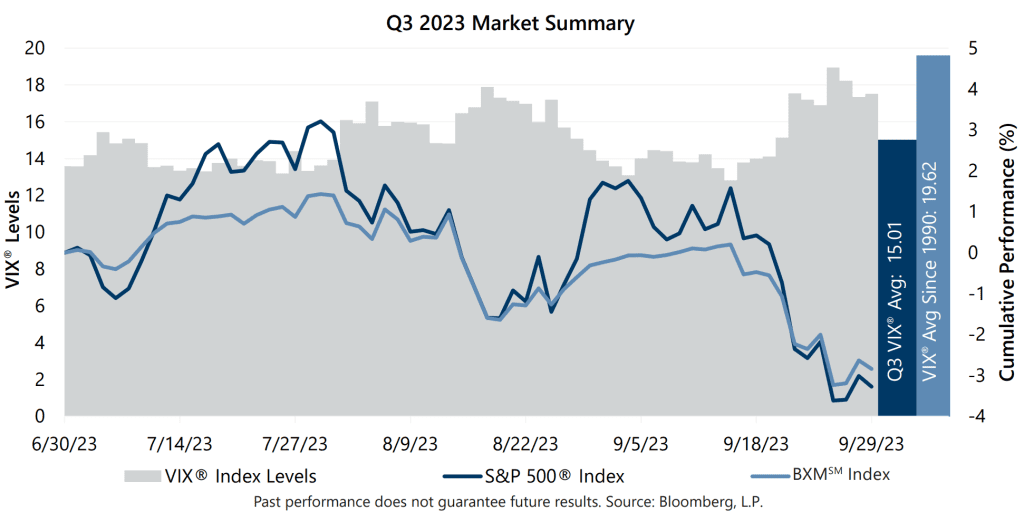

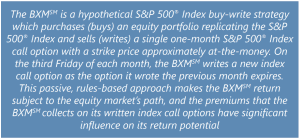

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -2.84% in the third quarter, holding up better than the S&P 500® Index and bringing its year-to-date return to 7.33%. The BXMSM returned 1.43%, -1.58% and -2.67% in July, August and September, respectively. The premiums the BXMSM collected as a percentage of the BXM’sSM underlying value were 1.39%, 1.91% and 1.63% in July, August and September, respectively.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -2.84% in the third quarter, holding up better than the S&P 500® Index and bringing its year-to-date return to 7.33%. The BXMSM returned 1.43%, -1.58% and -2.67% in July, August and September, respectively. The premiums the BXMSM collected as a percentage of the BXM’sSM underlying value were 1.39%, 1.91% and 1.63% in July, August and September, respectively.

The equity market advance in July positioned the BXMSM to enter August with relatively low market exposure. This passive position was beneficial, providing 163 basis points (bps) of protection, during the equity market decline from the end of July through August 18. The BXMSM wrote a new index call option in August, resetting its market exposure, but this wasn’t enough to keep pace with the equity market’s late-month rally. Remaining premium from August’s written index call option combined with premium collected in September helped provide 217 bps of downside protection during September’s market decline.

The Bloomberg U.S. Aggregate Bond Index (the Agg) returned -3.23% in the third quarter as interest rates continued their ascent. The Agg has had a rough go in 2023, concluding a five-month losing streak in September with a year-to-date return of -1.21%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended the second quarter at 3.84% before reaching an intra-quarter low of 3.75% in July. The 10-year yield then rose to reach an intra-quarter high of 4.61% on September 27 before closing September at 4.57%. The yield on the 2-year U.S. Treasury Note exceeded that of the 10-year for the entire quarter, an inversion of its typical relationship that has persisted since July 5, 2022.