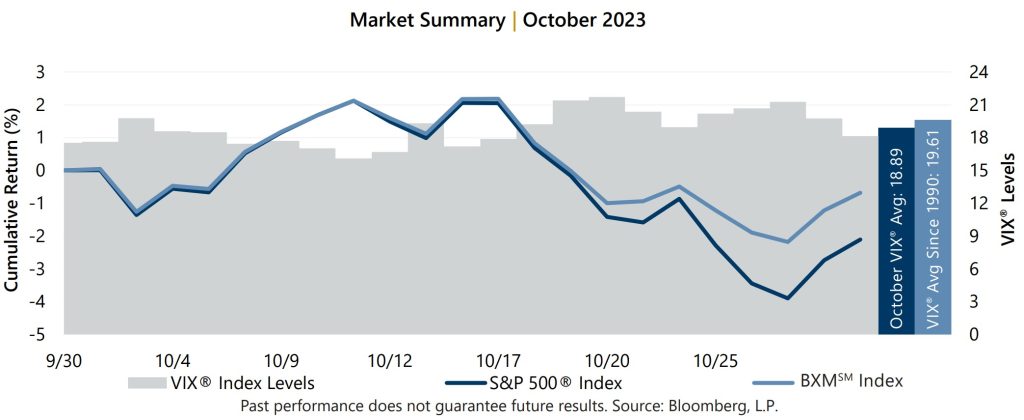

The equity market decline in September positioned the BXMSM to enter October with relatively high market exposure. This passive positioning proved beneficial during the market advance from September 30 through October 11, during which the BXMSM returned 2.13% compared to the 2.12% return of the S&P 500® Index. The BXMSM wrote a new index call option in October, resetting its market exposure amidst a decline and collecting a premium of 2.21%. This option writing premium contributed to 168 basis points (bps) of downside protection during the equity market’s intra-month decline from October 11 to October 27. The BXMSM returned -4.22% compared to the S&P 500® Index return of -5.90% during the period. The BXMSM returned -6.30% during the 2023 equity market max drawdown from July 31 to October 27 as option writing premiums contributed to the 364 bps of downside loss mitigation relative to the S&P 500® Index decline of -9.94%.

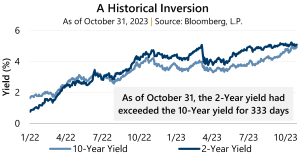

The Bloomberg U.S. Aggregate Bond Index (the Agg) returned -1.58% in October as interest rates continued to climb and the feeling of “higher-for-longer” seemed to settle-in. The Agg has had a rough go in 2023, concluding a six-month losing streak in October with a year-to-date return of -2.77%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended September at 4.57% before reaching an intra-month low of 4.56% on October 11. The 10-year yield then rose to reach a 2023 high of 4.99% on October 19 before closing the month at 4.93%. In a historical inversion that has persisted since July 5, 2022, the yield on the 2-year U.S. Treasury Note exceeded that of the 10-year for the month.

The Bloomberg U.S. Aggregate Bond Index (the Agg) returned -1.58% in October as interest rates continued to climb and the feeling of “higher-for-longer” seemed to settle-in. The Agg has had a rough go in 2023, concluding a six-month losing streak in October with a year-to-date return of -2.77%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended September at 4.57% before reaching an intra-month low of 4.56% on October 11. The 10-year yield then rose to reach a 2023 high of 4.99% on October 19 before closing the month at 4.93%. In a historical inversion that has persisted since July 5, 2022, the yield on the 2-year U.S. Treasury Note exceeded that of the 10-year for the month.