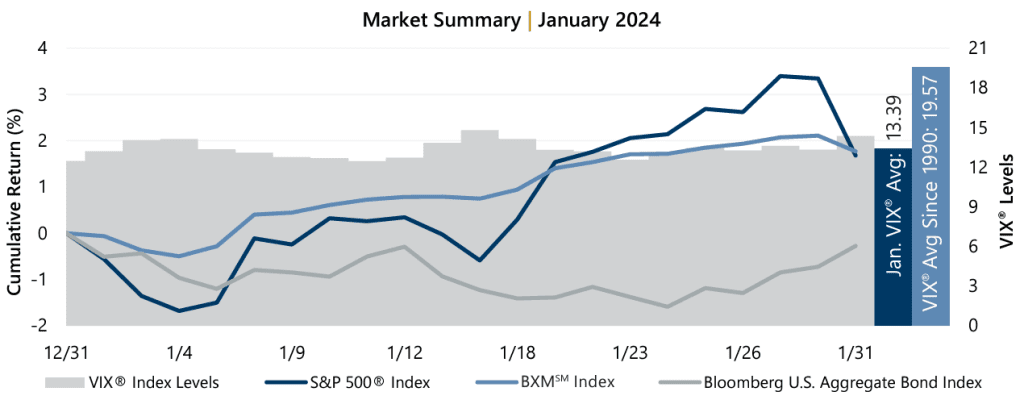

The equity market rally from the end of 2023 carried into January, although not without bumps along the way. From the start of the year to January 4, the equity market declined 1.68% before resilient economic data and ongoing optimism surrounding the expectation for interest rate cuts fueled a 5.16% advance from January 4 through January 29. Month-end comments from the U.S. Federal Reserve (the Fed), however, dampened the outlook for immediate cuts and renewed concerns over monetary policy. This resulted in the S&P 500® Index’s largest daily decline since September 2023 which contributed to a -1.66% decline from January 29 to month-end.

The equity market rally from the end of 2023 carried into January, although not without bumps along the way. From the start of the year to January 4, the equity market declined 1.68% before resilient economic data and ongoing optimism surrounding the expectation for interest rate cuts fueled a 5.16% advance from January 4 through January 29. Month-end comments from the U.S. Federal Reserve (the Fed), however, dampened the outlook for immediate cuts and renewed concerns over monetary policy. This resulted in the S&P 500® Index’s largest daily decline since September 2023 which contributed to a -1.66% decline from January 29 to month-end.

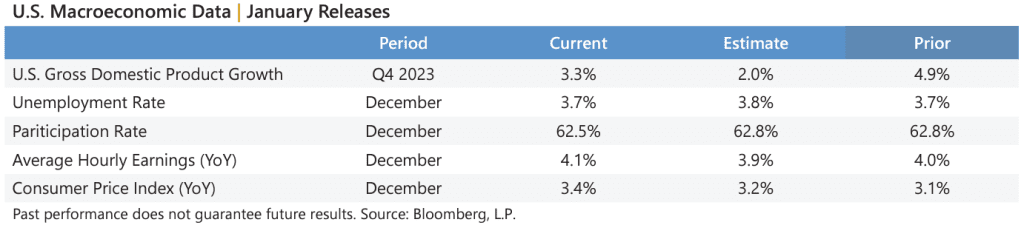

Macroeconomic data released during January showed a resilient economy and stubborn inflation, running contrary to hopes that the Fed would see that its tightening efforts have done plenty to cool the economy and conquer runaway inflation. The first estimate of Gross Domestic Product for the fourth quarter of 2023 showed a deceleration from the prior reading but well above the consensus estimate. Meanwhile, the December Consumer Price Index released January 11 showed an unexpected increase in the year-over-year figure. Corporate earnings reflected continued resilience as well, with fourth quarter aggregate operating earnings on track to climb 1.1% quarter-over-quarter and 7.8% year-over-year. With over 36% of S&P 500® Index companies reporting, nearly 82% met or exceeded analyst estimates.