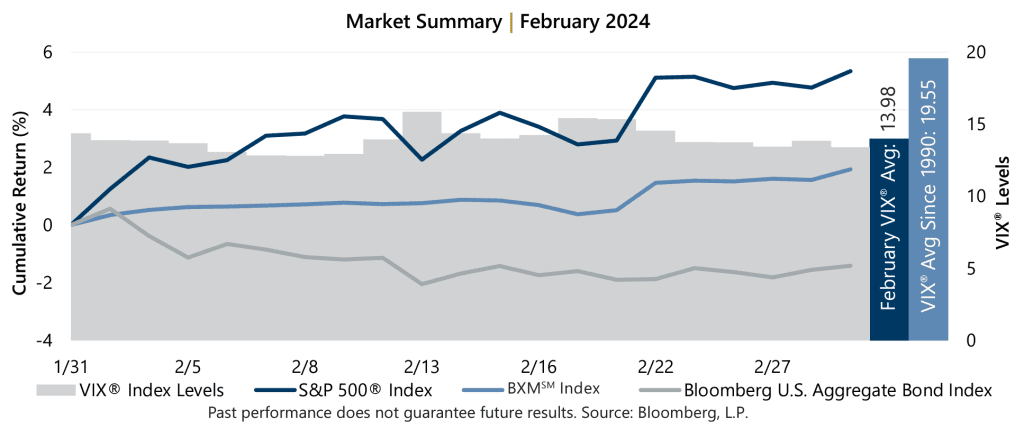

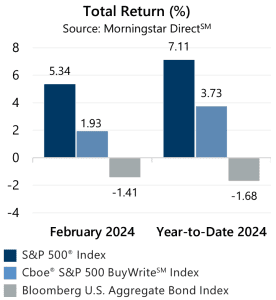

The equity market’s 5.34% rally during February led the S&P 500® Index to close the month at an all-time high. From the start of the year to February 29, the equity market has climbed 7.11%. The market’s advance has been fueled by an AI-related tech boom, but also a persistent optimism that the U.S. Federal Reserve will view its efforts to tackle runaway inflation as successful and feel comfortable enough to lower rates, potentially multiple times, during 2024.

The equity market’s 5.34% rally during February led the S&P 500® Index to close the month at an all-time high. From the start of the year to February 29, the equity market has climbed 7.11%. The market’s advance has been fueled by an AI-related tech boom, but also a persistent optimism that the U.S. Federal Reserve will view its efforts to tackle runaway inflation as successful and feel comfortable enough to lower rates, potentially multiple times, during 2024.

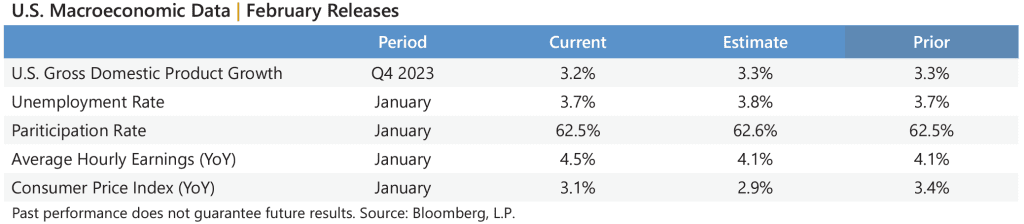

Macroeconomic data released during February showed a resilient economy and stubborn-but-softer inflation. The second estimate of Gross Domestic Product for the fourth quarter of 2023 showed a deceleration from the prior reading and just below the consensus estimate. The January Consumer Price Index released February 13 was lower than the previous reading but stubbornly above consensus estimates. Corporate earnings reflected continued resilience as well, with fourth quarter aggregate operating earnings on track to climb 1.8% quarter-over-quarter and 8.5% year-over-year. With over 96% of S&P 500® Index companies reporting, nearly 79% met or exceeded analyst estimates.