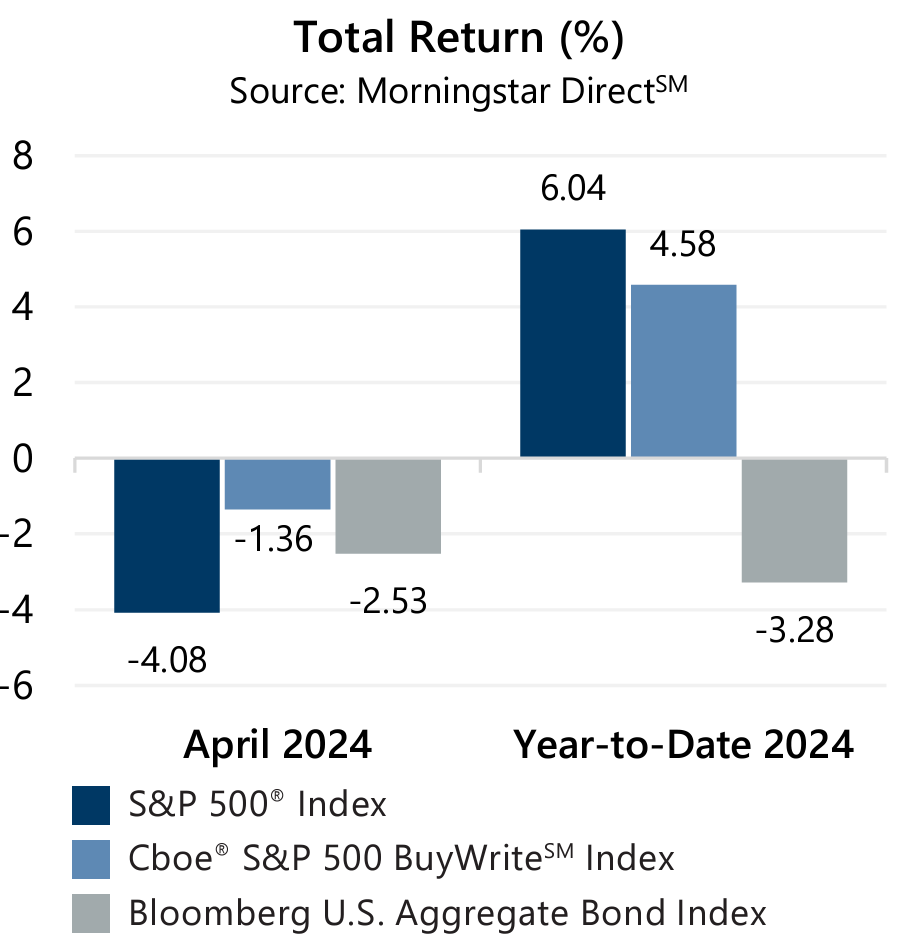

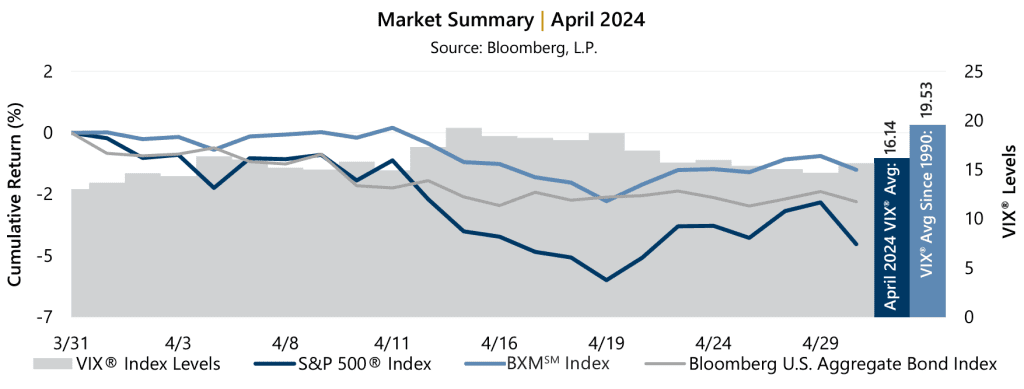

The equity market was challenged in April as economic data and stickier than expected inflation pushed the U.S. Federal Reserve (the Fed) further away from prior suggestions that interest rate cuts would be appropriate in 2024. April marked the first monthly decline for the S&P 500® Index since October 2023. From the close of March through April 19, the S&P 500® Index booked a new year-to-date maximum drawdown of 5.40% before attempting to recover before month’s end. From April 19 to April 29, the S&P 500® Index climbed 3.01%. However, the equity market ended the month on a sour note and declined 1.57% on the last day of the month, April 30.

The equity market was challenged in April as economic data and stickier than expected inflation pushed the U.S. Federal Reserve (the Fed) further away from prior suggestions that interest rate cuts would be appropriate in 2024. April marked the first monthly decline for the S&P 500® Index since October 2023. From the close of March through April 19, the S&P 500® Index booked a new year-to-date maximum drawdown of 5.40% before attempting to recover before month’s end. From April 19 to April 29, the S&P 500® Index climbed 3.01%. However, the equity market ended the month on a sour note and declined 1.57% on the last day of the month, April 30.

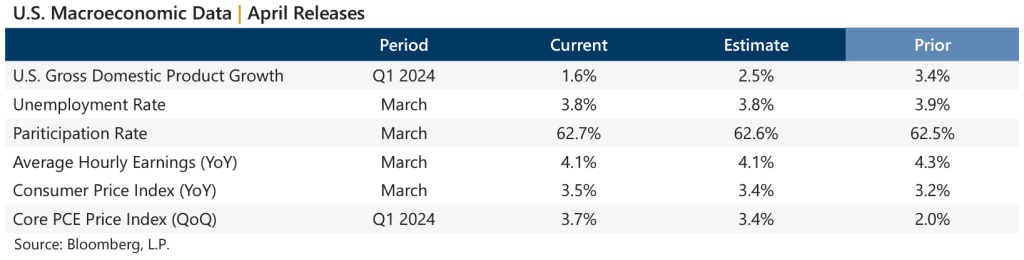

Data released in April showed a softening macroeconomic backdrop with stubborn inflation. The first estimate of Gross Domestic Product for the first quarter of 2024 was a significant deceleration from the prior quarter and well below the consensus estimate. The year-over-year March Consumer Price Index, released April 10, was higher than the previous reading and above consensus estimates. The quarter-over-quarter PCE Price Index, a Fed favorite, showed an increase of 3.7%, outpacing the prior reading and consensus expectations. Corporate earnings showed some resilience, with first quarter aggregate operating earnings on track to climb 1.3% quarter-over-quarter and 8.1% year-over-year. With just under 57% of S&P 500® Index companies reporting, nearly 83% have met or exceeded analyst estimates.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -1.36% in April, bringing its year-to-date return to 4.58%. The premiums the BXMSM collected as a percentage of its underlying value provided downside loss mitigation. After March’s equity market advance, the BXMSM entered April with relatively low market exposure which increased until the market’s April 19 low, at which time the BXMSM wrote its new index call option with a May expiration and reset its market exposure. From the close of March to April 19, the BXMSM offset 289 basis points of downside protection with a return of -2.51% relative to the -5.40% decline of the S&P 500® Index. The BXMSM collected a premium of 1.72% when writing its new index option on April 19, which supported returns through the remainder of the month. From April 19 to month-end, the BXMSM returned 1.18% while the S&P 500® Index returned 1.39%.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned -1.36% in April, bringing its year-to-date return to 4.58%. The premiums the BXMSM collected as a percentage of its underlying value provided downside loss mitigation. After March’s equity market advance, the BXMSM entered April with relatively low market exposure which increased until the market’s April 19 low, at which time the BXMSM wrote its new index call option with a May expiration and reset its market exposure. From the close of March to April 19, the BXMSM offset 289 basis points of downside protection with a return of -2.51% relative to the -5.40% decline of the S&P 500® Index. The BXMSM collected a premium of 1.72% when writing its new index option on April 19, which supported returns through the remainder of the month. From April 19 to month-end, the BXMSM returned 1.18% while the S&P 500® Index returned 1.39%.

The Bloomberg U.S. Aggregate Bond Index returned -2.53% in April, bringing its year-to-date return to -3.28%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended March at 4.20% and hit an April low of 4.31% on April 1. As the Fed dialed back hopes of rate cuts, the yield on the 10-year climbed to a 2024 high of 4.70% on April 25 before closing the month at 4.68%. In a historical inversion that has persisted since July 5, 2022, the yield on the 2-year U.S. Treasury Note exceeded that of the 10-year for the month.