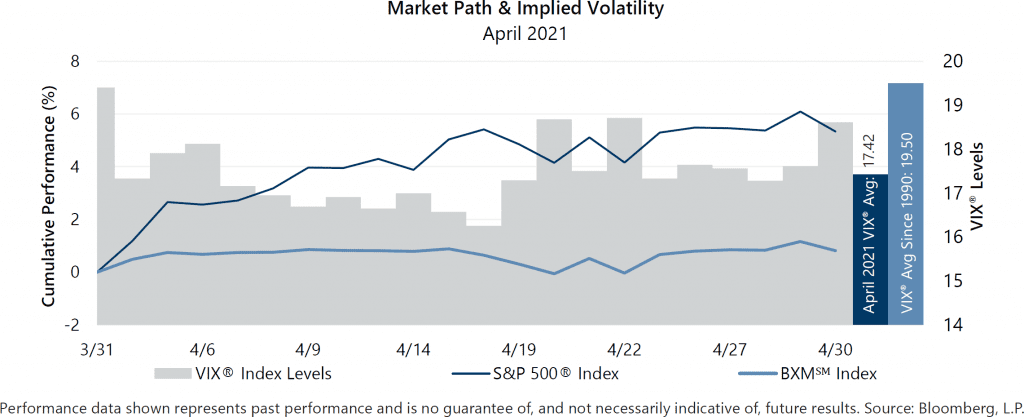

The S&P 500® Index climbed 5.34% for the month of April, bringing its year-to-date return to 11.84%. Positive U.S. macroeconomic data and continued improvement in pandemic-related statistics in the U.S. fueled the rally.

Macroeconomic data released in April continued to reflect positive trending developments in the U.S. The first estimate of Gross Domestic Product for the first quarter of 2021 showed that the U.S. grew at an annualized rate of 6.4%, in line with the consensus expectation. The unemployment rate continued to decline from 6.2% in February to 6.0% in March, matching the consensus expectation, while the participation rate ticked up to 61.5%. Inflation came in higher than expected, as the March Consumer Price Index, released on April 13, showed a 2.6% year-over-year increase which was above the average consensus estimate. With nearly 59% of companies reporting, first quarter aggregate operating earnings were on track to climb 21.48% quarter-over-quarter while declining 2.87% year-over-year. More than 88% of the companies that reported earnings met or exceeded analyst estimates.

Implied volatility, as measured by the Cboe® Volatility Index (the VIX®), averaged 17.42 in April. Consistent with its normal relationship, average implied volatility exceeded realized volatility, as measured by the standard deviation of daily returns for the S&P 500® Index, which was 10.84% for the month. The VIX® opened the month at 17.33 and drifted to an intra-month low of 16.25 on April 16 before climbing to its intra-month high of 18.71 on April 22. The VIX® closed the month at 18.61.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 0.81% in April, underperforming the S&P 500® Index by 453 basis points (bps) and bringing its year-to-date return to 6.60%. On the third Friday of each month, the BXMSM writes a new index call option as the option it wrote the previous month expires. The premiums the BXMSM collects on its written index call options have significant influence on its return potential during market advances and help to mitigate market declines. With a strong market advance during the final week of March, the BXMSM entered April with very little equity market exposure and time premium to earn remaining on its call option that was written in March. From the beginning of April through April 15, the BXMSM returned 0.88% which was not nearly enough to keep pace with the rapid advance of the equity market as the BXMSM lagged the 5.03% return of the S&P 500® Index by 415 bps during this time period. On April 16, the BXMSM wrote a new index call option with a May expiration as its April option expired. The premium collected on the new index call option as a percentage of the BXM’sSM underlying value was 1.51% and helped the BXMSM provide downside protection and outperform the S&P 500® Index from April 16 through month-end as the BXMSM returned 0.18% relative to the S&P 500® Index return of -0.07%.

The Bloomberg Barclays U.S. Aggregate Bond Index returned 0.79% in April, bringing its year-to-date return to -2.61%. The yield on the 10-year U.S. Treasury Note (the 10-year) started April at 1.67% before climbing to its intra-month high of 1.72% on April 2. The 10-year then drifted to an intra-month low of 1.54% on April 22 before closing the month at 1.63%.

1The BXMSM is a passive total return index designed to track the performance of a hypothetical buy-write strategy on the S&P 500® Index. The construction methodology of the index includes buying an equity portfolio replicating the holdings of the S&P 500® Index and selling a single one-month S&P 500® Index call option with a strike price approximately at-the-money each month on the Friday of the standard index-option expiration cycle and holding that position until the next expiration.

Sources: Morningstar DirectSM, Bloomberg, L.P. Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results.

For more information and access to additional insights from Gateway Investment Advisers, LLC, please visit www.gia.com.