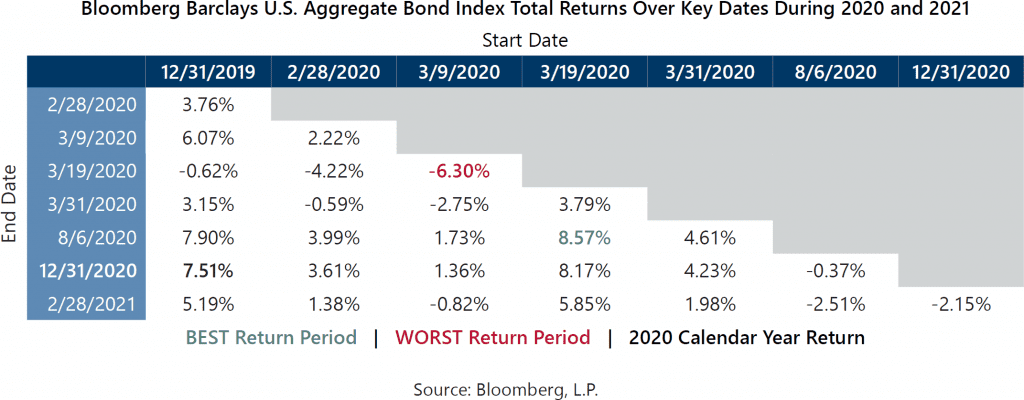

After posting strong returns in 2019 and 2020, inflation concerns have driven the Bloomberg Barclays U.S. Aggregate Bond Index (the Agg) to a loss of 2.15% on a year-to-date basis through February. The bond market is off to a worse start in 2021 than it had in 2018, a year in which the Agg had a total return of just one one-hundredth of one percent.

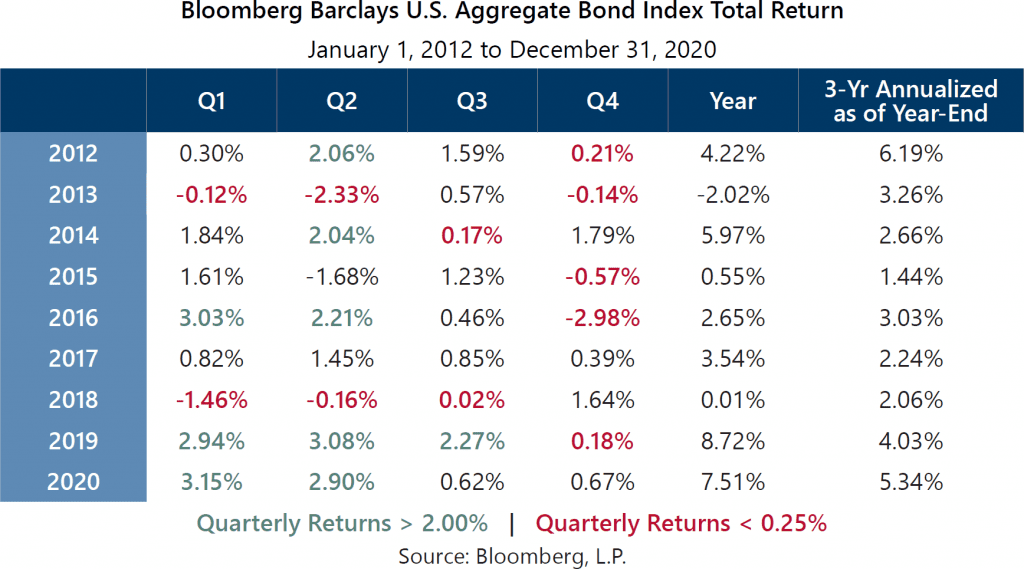

The 2020 return for the Agg gives the impression that it was a good year for bonds; however, the chart and table below reveal that the year unfolded like a play – with a good opening act that leaves the audience wishing they had left at intermission. Bond investments in place at the beginning of 2020 earned attractive returns relative to what bonds have produced in recent years, but bond investments made after March 2020 have produced much lower returns. Moreover, post-March bond investments have come at an enormous opportunity cost given how strong equity market returns have been since the equity market bottomed in March 2020.

It is worth noting that investor demand for bonds increased after March 2020. Net flows into domestic bond mutual funds and exchange traded funds in the last nine months of 2020 totaled nearly $500 billion dollars, 2% above the full-year total for 2019 and nearly 70% higher than 2012, the next highest annual total in the previous 10 years.

Short spurts of high returns followed by low or negative returns is a pattern that has been in place for a number of years. While the trend of declining longer-term annualized returns for the Agg was interrupted by plummeting interest rates in response to the pandemic, the downward trend in longer-term bond market returns may likely resume unless another crisis drives interest rates back down.

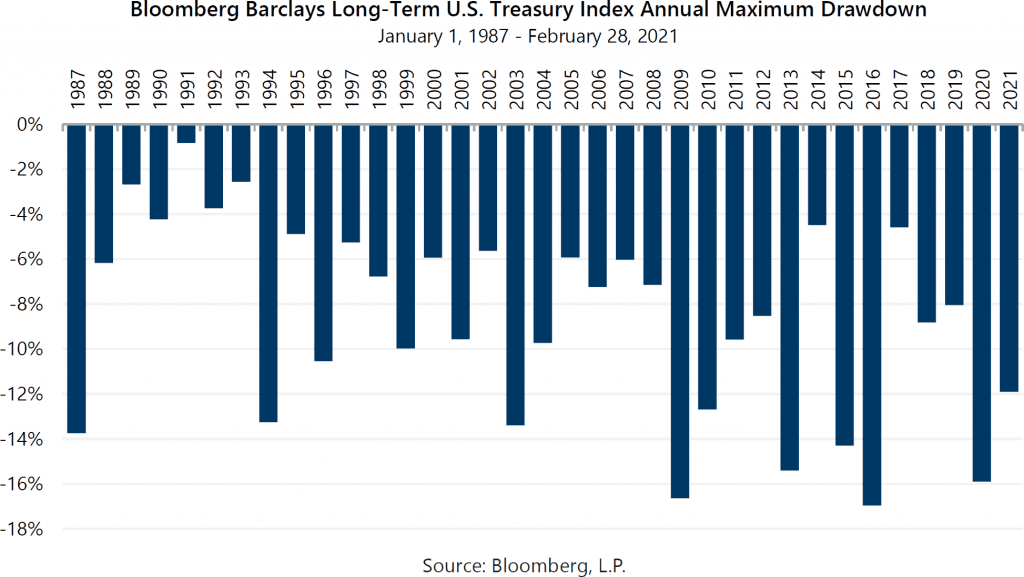

In addition to the potential for low long-term returns, an increased frequency of sharp losses has also emerged as a characteristic of the bond market during low interest rate periods. This phenomenon was particularly visible in long-term government bonds. The nearly 12% drawdown for the Bloomberg Barclays Long-Term U.S. Treasury Index from the beginning of 2021 through February 25 was the 11th double-digit intra-year drawdown for the index since 1987. Such large losses used to be rare, but the 2021 drawdown was the seventh double-digit loss since 2009.

The current environment of high equity market valuations and low interest rates amplifies the challenge of keeping a diversified portfolio positioned for long-term growth while guarding against potential equity market losses. In this unique set of circumstances, investors may benefit from becoming less reliant on high-quality fixed income instruments for lowering the risk of their portfolios. Incorporating other risk management strategies that have relatively attractive long-term return potential is a possible solution. Low-volatility equity strategies that rely on cash flow to both mitigate equity market losses as well as participate in equity market advances, like those managed by Gateway, may be a suitable alternative for investors who currently favor high-quality bonds to lower the risk of their portfolios. Gateway’s low-volatility equity strategies strategically and consistently seek to reduce the risk of their underlying equity exposure, creating the potential to limit losses during equity market declines and capture a majority of the long-term return of the equity market with lower risk.

*For more information and access to additional insights from Gateway Investment Advisers, LLC, please visit www.gia.com/insights.