What is the role of low-volatility investments – such as option writing strategies – if equity market volatility persists at the levels seen in November? Despite several potential sources of market aggravation, equity market volatility drifted to a year-to-date low in November. Congressional impeachment hearings seemed to further entrench the nation’s partisan divisions. Progress toward a resolution of the U.S.-China trade war was uneven and uncertain at best. Unrest in some of the world’s least restful areas, including Hong Kong and Iran, intensified. And the U.K. dissolved Parliament in advance of a general election that may finally decide if and how Brexit happens.

With these significant outside forces threatening to disturb market tranquility, what forces helped keep a damper on market volatility recently? Solid domestic economic data releases and very few Q3 earnings disappointments may have helped. The Federal Reserve (the Fed) likely played a role as well—their third rate cut in October seemed to get their policy rate caught-up with market expectations. At month-end, bond futures market pricing implied a sub-50% probability for additional rate adjustments over the first half of 2020. Furthermore, the Fed has resumed growing its balance sheet. It is doing this in an effort to facilitate the smooth function of the overnight repurchase market after a brief but volatility-inducing hiccup in September. From the end of August to the end of November, the Fed’s balance sheet grew by nearly $300 billion, undoing almost all the balance sheet reduction that had occurred over the first eight months of 2019.

The market environment of November was reminiscent of 2017 when threats to market quietude were numerous – but unrealized – and volatility readings were persistently at or near record lows. While recent volatility readings remain above those seen in 2017, a return of market resilience to potential volatility triggers is a good reason to revisit the role of option writing strategies and performance expectations in a low volatility environment.

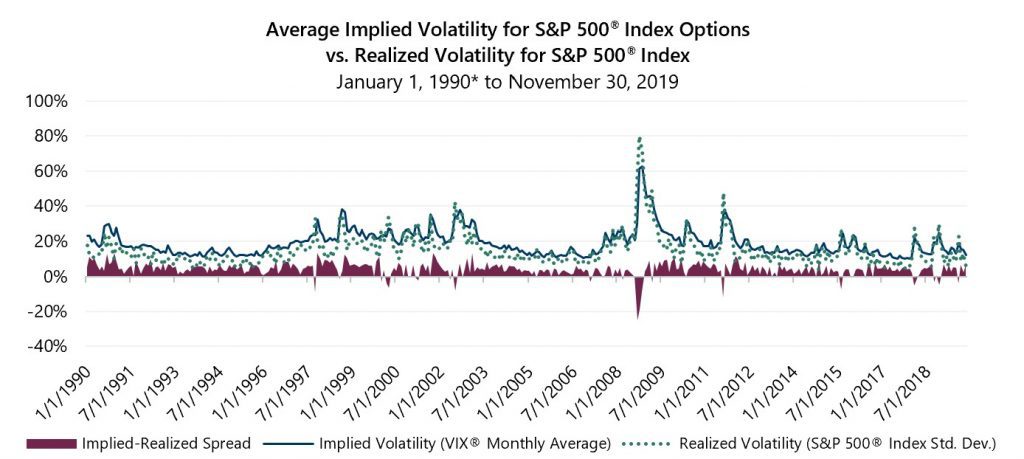

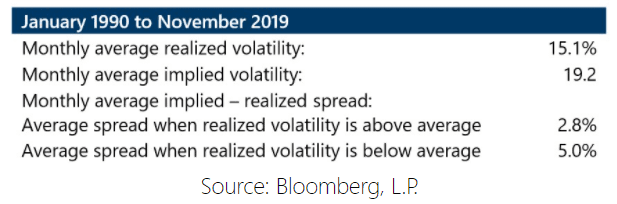

Index option writing strategies and their associated indexes, like the Cboe® S&P 500 BuyWriteSM Index1 and Cboe® S&P 500 PutWriteSM Index2, have shown potential for consistent risk-reduction relative to the broader equity market. The investment role of such strategies typically is not predicated upon outperforming the equity market over the short-term, but to exhibit a lower risk level than the equity market while benefitting from the propensity of the market to rise over time. Moreover, option writing strategies typically focus on the potential to deliver better risk-adjusted returns over the long term than equity-only strategies through exposure to the volatility risk premium (VRP). VRP expresses itself in index option markets through the pricing of implied volatility relative to the realized volatility the index experiences. As the graph below illustrates, Cboe® Volatility Index (the VIX®) levels are frequently and consistently priced above the realized volatility the S&P 500® Index experiences.

The overpricing of the implied volatility component of index option prices creates the potential for strategies that write, i.e. sell, options to deliver improved risk-adjusted return relative to the equity indexes associated with such strategies over the long term. The wider and more consistent the spread between implied and realized volatility is, the more potential exists for improved risk-adjusted return from option writing.

Low-volatility environments have historically been associated with a higher VRP. In other words, the spread between implied and realized volatility has tended to be higher in months when realized volatility was below average. Conversely, in months when realized volatility was above average, the spread between implied and realized has been lower. November was illustrative of this phenomenon with realized volatility coming in at just 5.77% and implied volatility averaging 12.52, a well-above-average spread of nearly seven points.

A continuation of richer-than normal option pricing combined with low realized volatility creates the potential for option writing strategies to deliver attractive risk-adjusted returns with lower-than normal volatility. Attractive risk-adjusted returns never go out of style and, in the current environment of low interest rates with the potential to rise over time, there are potential advantages to seek them through allocations to option writing strategies. If low or rising interest rates keep bond market returns low, diversified investors may benefit from investments that do not have interest rate sensitivity and can complement bonds’ historical profile of low volatility and attractive risk- adjusted returns. For investors who anticipate that recent market tranquility is temporary, option writing strategies that seek to consistently deliver lower risk and less downside than the equity market may be an appealing way to reduce equity market exposure and risk. In either application, option writing exposure to the VRP has the potential to generate attractive risk-adjusted returns over the long-term.

1The Cboe® S&P 500 BuyWriteSM Index (the BXMSM) is a passive total return index designed to track the performance of a hypothetical buy-write strategy on the S&P 500® Index. The construction methodology of the index includes buying an equity portfolio replicating the holdings of the S&P 500® Index and selling a single one-month S&P 500® Index call option with a strike price approximately at-the-money each month on the Friday of the standard index-option expiration cycle and holding that position until the next expiration.

2The Cboe® S&P 500 PutWriteSM Index (the PUTSM) is a passive total return index designed to track the performance of a hypothetical portfolio that sells S&P 500® Index (SPX) put options against collateralized cash reserves held in a money market account. The PUTSM strategy is designed to sell a monthly sequence of SPX puts and invest cash at one- and three-month Treasury Bill rates. The monthly sequence entails writing one-month SPX put options with a strike price approximately at-the-money each month on the Friday of the standard index option expiration cycle and holding that position until the next. The number of put contracts with identical strike prices and expiration dates sold varies from month to month but is limited so that the amount held in Treasury Bills can finance the maximum possible loss from final settlement of the SPX puts.